Macro Monitor

RAI Falls, But Stays On “Higher Risk” Signal—Remain Cautious

The RAI fell in August and stayed on a “High Risk” signal. We remain cautious and recommend higher quality within fixed income.

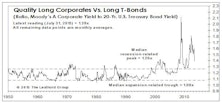

U.S. Investment Grade Corporate Bonds: Maintain Favorable

This is consistent with our overall cautious view on credits. Credit spreads continued narrowing despite higher volatility in the bond markets.

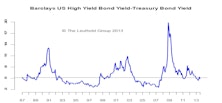

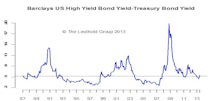

U.S. High Yield Corporate Bonds: Maintain Neutral

On the positive side, the fundamental picture is still healthy for most U.S. high yield issuers, and defaults are expected to be low. On the negative side, weakening inflation expectations is a divergence that bears close monitoring. We will exercise patience and wait for a better entry point.

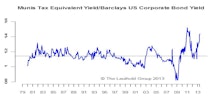

U.S. Municipal Bonds: Maintain Neutral

Their relative cheapness, combined with the prospect of higher tax rates, certainly makes Munis more attractive now. But we’ll wait for interest rate volatility and outflows to subside before turning bullish on Munis.

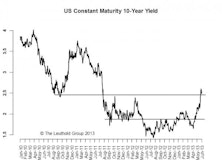

10-Year: Taper the Taper—Upside Limited

If interest rates keep going higher from here, we would run the risk of derailing a still-fragile recovery. As long as the Fed tapering uncertainty exists, we expect higher volatility on the 10-year yield to persist in the mean time.

The Dollar: Upside Limited In The Near Term

A closer look at the dollar’s two main counterparts, the euro and the yen, reveals a regime shift in both cases, but for different reasons.

RAI Fell, But Stayed On “Higher Risk” Signal—Remain Cautious

The RAI fell in July and stayed on a “High Risk” signal. We remain cautious and recommend higher quality within fixed income.

U.S. Investment Grade Corporate Bonds: Maintain Favorable

Despite the exodus from all bond classes in the last few months, longer term demand for safe spreads is likely to remain strong and investment grade issuance has dropped significantly.

U.S. High Yield Corporate Bonds: Maintain Neutral

Over the past few months we’ve seen the largest high yield bond fund outflow since 2000. We will exercise patience for now and wait for a better entry point.

U.S. Municipal Bonds: Maintain Neutral

The relative cheapness combined with the prospect of higher tax rates certainly makes us much more interested in Munis now. But we’ll exercise patience, waiting for the negative headlines to fade and interest rate volatility to subside before turning bullish on Munis.

U.S. High Yield Corporate Bonds: Maintain Neutral

Although the fundamental picture remains healthy for most U.S. High Yield issuers and defaults are expected to be low, the reversal of a crowded trade could lead to further substantial losses on these bonds.

U.S. Municipal Bonds: Maintain Neutral

We believe the sell-off in Munis is overdone in the short-term and these bonds look attractive relative to Treasuries. But in the medium-term the tapering risk will linger; this is a big negative for long maturity credits like Munis.

U.S. Investment Grade Corporate Bonds: Maintain Favorable

The longer term demand for safe spreads is likely to remain strong once yields normalize and volatility recedes.

RAI Rises Again, Stays On “Higher Risk” Signal—Remain Cautious

The RAI rose again in June and stays on a “High Risk” signal. June saw an acute case of carry trade reversal; we remain cautious and recommend higher quality within fixed income.

10-Year: 185-245 Range Broken & Higher Volatility

We think 3% is the upper bound in the short term. However, we believe it will settle back closer to 250 bps by the end of the year.

Time Cycle Composite Mid-Year Update—More Volatility & Lower Returns in H2

For the first half of the year, QE tapering disrupted the usual patterns for most interest rate related markets but equities are largely on track. In the second half, the common message seems to be higher volatility and lower returns.

Long U.S. Treasuries: Big Move In May, Downside Still Significant

20 Year T-Bond: 5 3/8’s, Maturity: 2/15/2031, YTM 2.88% (vs. April 30th YTM at 2.39%)

U.S. High Yield Corporate Bonds: Maintain Neutral

High yield bonds are not immune to the tapering of QE.

U.S. Municipal Bonds: Maintain Neutral

Inflows into Muni bond funds turned negative; higher interest rates currently the biggest risk.

U.S. Investment Grade Corporate Bonds: Maintain Favorable

Consistent with our overall cautious view on credits, we still like “safe spreads”.