Macro Monitor

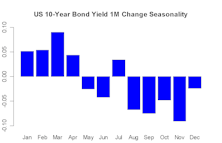

10-Year Yield: 250-280 Range Intact

As we expected, at 250-270, the 10-year yield stayed within our narrow target range in June.

Time Cycle Composite—Mid-Year Update

Our beginning-of-the-year message—“lower your expectations and be patient” has largely been true so far this year as most equity markets tracked the historical pattern pretty closely.

Risk Aversion Index - Stayed On Higher Risk Signal

The level of this index is in an extreme zone where false alarms are more likely as small movements in the index can trigger new signals.

10-Year Yield: Back in 250-280 Range

In the very short term, excessive bearish positions have been reversed so there is less downside pressure on interest rates. Over the intermediate term, incredibly low yields in the Euro-zone help cap the U.S. yield.

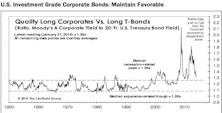

Credit Conditions Still Good But Less-Easy Than Pre-Taper

With the Taper underway and the back-up in interest rates over the last year, credit conditions have become less-easy for some consumers and small businesses.

Risk Aversion Index - New Higher Risk Signal

Surprising strength in the Yen, a drop in commodities, and slightly wider credit spreads pushed up the index. An increase in risk aversion becomes more likely at the current extremely low level. Caution is warranted.

US Bond Market

Although the overall picture remains favorable for high grade credits, the increased exposure to interest rates with an ever thinner spread cushion does concern us. We will monitor closely for potential downgrades.

10-Year Yield: More Downside

We expect the 245-250 barrier to be tested, and if it is decisively broken, much lower yields could be in the cards.

Sell in May

This does not only apply to stocks, it applies to just about all risky assets.

Twisty Curves

The short end of the yield curve sold-off to price in an earlier-than-expected rate hike, while the long end rallied as the prospect of tightening reduced longer-term inflation expectations.

RAI Lower - Stays on "Lower Risk" Signal

Risk assets continued to perform well in March, and our monthly Risk Aversion Index (RAI) fell to near record low levels. We continue to favor high quality credits within fixed income.

RAI Falls Sharply—New “Lower Risk” Signal

This closed out the one month old “Higher Risk” signal. We continue to favor high quality credits within fixed income.

Have We Seen This Post-QE Movie Before? It’s Still Too Early To Call

We looked at the periods around the end of the three previous easing programs (QE1, QE2 and Operation Twist) and compared those patterns with the current ones for various measures. The current patterns from both an economic and a market front bear enough resemblance to the previous ones to make us a bit uncomfortable. February’s market action was encouraging, but it is still too early to rule out a post-QE fizzle.

U.S. Bonds

Given the higher volatility and increased risk aversion, high grade credits are attractive as the negative relationship between rates and credit spreads dampens the volatility of this asset class.

Risk Aversion Index Turns Higher, New “Higher Risk” Signal

We are turning defensive within fixed income and recommend moving up the quality scale.