Macro Monitor

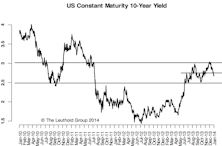

U.S. 10-Year: 245-250 Area A Strong Barrier

We expect the 245-250 area, the upper bound of the previous lower range, to be a strong barrier.

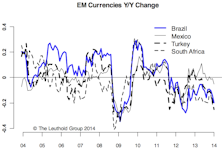

Can The EM Problem Spread To DM? Yes, If It Gets Bad Enough

The current EM weakness is not yet a full-blown crisis but, if it does become one, it will drag down developed economies too.

A Taper & Hibernating Bears

The rise in interest rates after the taper was on the back of low liquidity around the holidays. 3% is a pretty strong upper bound for the 10-year, and a failure to stay above this level will probably see a re- test of the 275 level in the near term.

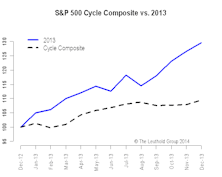

2014 Time Cycle—Lower Your Expectations & Be Patient

It’s time to update our time cycle composites, and what they say for equities in the U.S., U.K., Germany and Japan and long-term interest rates and credit spreads in the U.S.

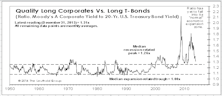

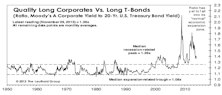

U.S. Bonds

The thin liquidity likely magnified the move in both rates and credit spreads, but we continue seeing a friendly macro environment that supports high quality credits.

US Bond Grades

The renewed participation of credits in the risk asset rally is a welcome sign.

Risk Aversion Index Edges Lower, Stays On Its “Lower Risk” Signal

We are in the seasonally favorable part of the year and we continue favoring high-grade credits within fixed income.

10-Year: No December Taper, Back To The 250 Level

Given our assumption of no December taper and the fact that most of the recent rise in interest rates is due to an early-taper fear, we expect the 10-year yield to drop back to the 250 level.

The Dual Mandate Presents A Clear Dilemma For The Fed

The “dual mandate,” which means the Fed is paying close attention to both inflation and employment, presents a clear dilemma for the Fed when it comes time to decide on a taper.

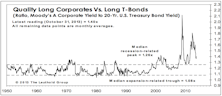

US Bond Market - October 2013

We are encouraged by the narrower spreads in October as the feared divergence between credits and equity markets did not continue.

Risk Aversion Index Falls Further, Stays On Its “Lower Risk” Signal

We seem to be in a “Goldilocks” period, where economic numbers are not bad enough to re-ignite recession fears but are just weak enough to push the taper farther off.

Five Reasons Inflation Is Still Missing

Overall demand slack, stubbornly low velocity of money, an overall stronger dollar, painfully low labor cost inflation and weakness in commodity prices are strong disinflationary forces.

10-Year: Year-End Target Still 250 BPS, Interim Volatility Expected

We don’t think the numbers between now and the Fed’s December meeting will be strong enough to convince it to start tapering this year. No taper until 2014, in our opinion.

Our Position on U.S. Bonds

U.S. Investment Grade Corporate Bonds: Favorable, U.S. High Yield Corporate Bonds: Neutral, U.S. Municipal Bonds: Neutral

Risk Aversion Index Falls To New “Lower Risk” Signal

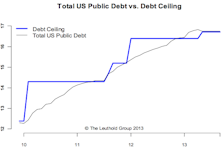

The RAI had the biggest drop of the year in September and triggered a new “Lower Risk” signal. This is largely due to the no-taper decision by the Fed. We remain cautious in the near term due to the debt ceil- ing debate but recommend increasing risky exposure after the debt ceiling resolution.

Inflation Still Going Nowhere In The U.S.

Inflation at both consumers’ and producers’ level is still modest. A drawn out government shutdown and debt ceiling debate will hurt the economy, which could further push out the taper timeline.

Debt Ceiling—Weakness Before But Strength After Resolution

A look at prior debt ceiling debates and patterns around resolution dates gives no surprises: markets are weaker in the two weeks before but stronger in the month after a resolution is reached.

No Taper—More Downside Likely On The 10-Year & Higher Volatility Ahead

A look at prior debt ceiling debates and patterns around resolution dates gives no surprises: markets are weaker in the two weeks before but stronger in the month after a resolution is reached.

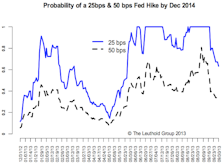

Data Dependency—September Taper Still Likely

More upside surprises are still likely and, despite the disappointing jobs report, the overall economic picture still supports a September taper. The improving economic picture is not just happening within the U.S., but in other major countries. We still believe the upside for the U.S. 10-year is limited.