Inside The Stock Market ...trends, cross-currents, and outlook

So Much For “Red October”

Now that the election is over and QE2 in the works, resist the temptation to “sell the news.” We expect to see the market rally through the end of the year. Sentiment still benign and valuations still attractive.

Playing The Bounce Update

Not much happening with this year’s edition of “Playing The Bounce.” Initial list of qualifiers posted a loss of 1% in October, while the S&P 500 was up 3.7%.

Housing Hangover: May Linger Longer Than You Think

Housing stocks, and the enablers that helped create the bubble (Financials), are following the usual pattern of busted bubbles. After the bust, these past bubbles typically see a beta bounce establishing post crash highs. After that, it can take many years before these highs are again broken.

Mining An Over-Correlated Stock Market

Correlations between asset classes have been running quite high over the last couple of years. Eric Bjorgen looks at current tightly correlated sectors that historically have not been so correlated.

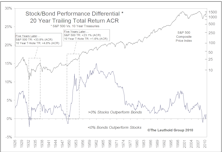

Slowly Righting The Ship Of Risk And Reward

Stock/bond Risk-reward relationship beginning to return to normal. Back in Q1 2009, performance differential between S&P 500 and 10 year T-bonds was at generational lows. In prior periods of bond superiority, stocks ultimately came soaring back. Expect to see stocks do much better over next 5 years.

Thoughts On Asia Investing: Performance & Valuation of Consumer Stocks

A look at Asian valuations show China to be fairly valued (neither overvalued nor undervalued), but there are other attractive (cheap) ways to play consumer stocks in Asia.

Back Aboard The Bull

Major Trend Index now Positive (both global and domestic). Even though we are bullish, there are several bullish arguments that we still don’t buy.

Beware The Economic Ticker Tape

It has become more and more difficult to filter out the short term economic noise. By focusing on this minutia, investors can easily lose sight of the big picture.

Pinpointing The True “Mean Season” For U.S. Stocks

We turn our attention to the domestic equity markets to determine where market history has hidden its seasonal landmines.

The 1974-1982 Template For Recovery

Current market recovery continues to track the post 1974 bear market recovery quite closely.

Major Trend More Bearish As Market Enters Historically Weakest Month

August turned out to be a very volatile month, not the “doldrums” that many investors would have wanted to see during this traditional summer vacation month. Budding optimism that had developed in investors back in April has now apparently been completely washed out by the poor August performance.

Will The Fabled Election Cycle Work Again?

Doug Ramsey looks at his own 15 month election cycle work to examine historical performance for a variety of different asset classes.

Lookback Blues… Still Depressing Long Term Equity Performance

It’s easy to see why equity investors are so down when looking at updates of the long term stock market performance. It’s even more depressing when long term equity returns are compared to bond returns.

Current Deflation Fears Are Unwarranted

Don’t fear deflation. Leuthold historical studies show mild deflation can actually be a good environment for the stock market.

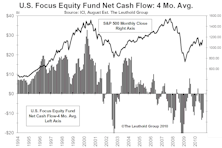

Basics For Fund Flow Trackers...And Exceptions To The Two Golden Rules

The relationship between equity mutual fund cash flow and performance of the equity markets can be reduced to two basic “golden rules” of interpretation.

Buckle Up For The “Doldrums”

Beware summer doldrums, August has a knack of sometimes being a crazy month. Market continues to be viewed as being in a severe correction mode, rather than a full fledged bear market.

Public Pensions—Changes Beginning

Last issue, we presented an introduction to our thoughts on the problems being faced by public pensions. The following is a look at some initial action by states.

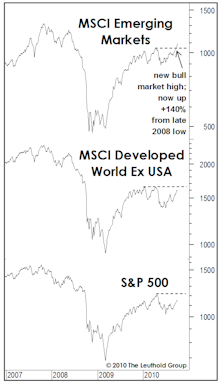

Going (More) Global

MSCI Index very undervalued, as the recovery off the March 2009 lows has left valuations still near prior bear market lows. Relative to foreign markets, the U.S. looks expensive. This is why we continue to maintain a healthy exposure to foreign stocks…especially emerging markets.

A Dissenting View On Materials

Per our work, sectors like Consumer Discretionary and Technology provide a better way to capitalize on the global recovery now underway.