Inside The Stock Market ...trends, cross-currents, and outlook

Are Public Pensions The Next Bubble?

Matt Paschke discusses how public pension funds are approaching huge hurdles as state and municipal governments have promised more than they are able to provide.

Major Trend Negative… Paring Stock Exposure

Major Trend Index has big decline in early July, bringing ratio all the way down to negative ground.

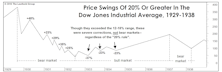

A Non-Economic Bear?

A market decline much beyond 20% could be labeled a “non-economic” bear market. Outstanding feature of past “non-economic” bear markets has been their brevity.

Stocks And Economy Joined At The Hip… For Now

Economic indicators are hypersensitive to even small changes in the data, and investors are hypersensitive to the indicators themselves.

Stock Market Reactions In Rising Tax Environment

Taxes are slated to go up as Bush tax cuts expire. History shows that selling increases in anticipation of higher capital gains taxes. Stock performance also does better in anticipation of lower tax environments than higher.

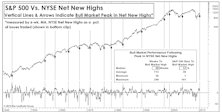

Here We Go Again?

Doug Ramsey looks at the history of “severe” market corrections (declines of 12% to 18%), and contrasts that with true bear markets.

Estimating The Upside: Yes, We Still See Some

Despite our still (cautiously) bullish outlook, historical P/E levels which once provided support to the stock market are expected to now offer resistance as the market moves higher.

Sunshine Ahead: Optimistic On Solar Sector

Here Comes The Sun! Read about Dave Kurzman’s outlook for the solar energy industry.

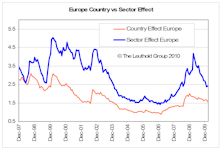

The Sector Effect vs. The Country Effect: A Region by Region Look

We examine the relative importance of country effect vs. sector effect within four regions: Europe, Eastern Europe/Middle East/Africa, Asia Pacific ex-Japan ex-China, and Americas ex-U.S.

The Sector Effect Vs. The Regional Effect

Focus of global investing has shifted from sector and is now centered on the regional effect.

Everyone Should Be A Supply Sider!

Analysts typically focus on demand for products and rarely look at the supply side. Consumer Discretionary companies were rewarded for their pessimistic positioning with better pricing and higher margins.

Putting Lipstick On The “PIIGS”

Global Industries equity portfolio has little to no exposure to the PIIGS (Portugal, Ireland, Italy, Greece, and Spain) as our Global Group Selection Scores have not led us to industries that have many component stocks domiciled in those countries. However, if this work leads us to groups with heavier exposure to the PIIGS, we’ll buy them without blinking.

An Open (Yet Purely Theoretical) Letter To Individual Investors

When you are all doing the same thing at the same time, it’s usually a good time to question if the investment makes sense anymore.

Quick Takes From The Valuation Dashboard

Stock market valuations no longer cheap, but they are also not yet truly expensive. Eric Bjorgen isolates several valuation measures to show just where they rank historically

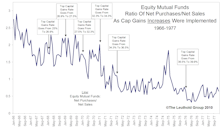

Liquidity Update: Trends Worth Watching

Helping propel the stock market recovery has been a build-up of excess liquidity. This has now generally been put to use, and can no longer be counted on as a market driver.

The Dreaded ‘Aha’ Moment

One of the great contrary trades in recent memory may well have been the Consumer Discretionary stocks during the last recession and early in the recovery. The consumer had been written off, but these stocks have been the clear market leader. It looks, however, like the move may be running out of steam.

Another Market Milestone

It is sobering to consider that an historic, 13-month market stampede (one now exceeding 75%) has done nothing more than restore the market to levels first seen twelve years ago.

Using A Few Bear Arguments To Make A Bullish Case

Doug Ramsey utilizes several bear market arguments to build a bullish case. Rising Interest Rates, Overbought Market, Low Volatility, and Low Trading Volumes, can all be looked upon in a BULLISH light.

The Higher Payout The Better: A Global Perspective on Dividends and Buybacks

This month Chung Wang examines historical performance of companies that increase or initiate dividends, as well as companies that are buying back stock. These stocks tend to significantly outperform.

Interest Rate Moves And Stock Prices… Another Look

At times it is indeed possible to have interest rates rise and stocks also move higher, and it is also possible to have rates decline and stocks fall.