Inside The Stock Market ...trends, cross-currents, and outlook

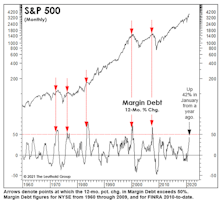

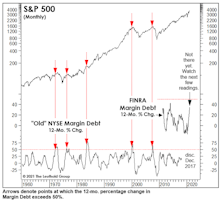

Lever Up!

Someday, we’ll have a chuckle with our (yet unborn) basketball-playing grandson about the time Shaquille O’Neal was able to raise several-hundred-million dollars in his second SPAC. But while these anecdotes get sillier and sillier, we have a personal bias toward speculative activity we can measure over time. That activity isn’t quite as alarming as the anecdotes, but it’s getting there.

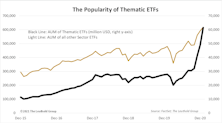

Newfound Popularity Of Thematic ETFs

We’ve noticed a small segment of equity ETFs, designated as “thematic,” that is increasingly gaining popularity. Thematic ETFs invest in baskets of stocks that share narrowly-defined business enterprises outside of the standardized GICS methodology.

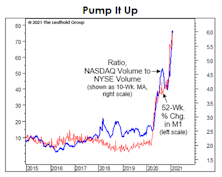

Silly Season

Move over, Y2K! In late January, the squeeze of popular hedge fund “shorts” eclipsed anything we saw at the peak of the Technology bubble. But who knows? An even wilder event might be in store in coming months.

Early-Cycle “Overheat?”

Equities continue to benefit from an odd combination of faith and doubt in the Federal Reserve: Faith that the “Fed put” under financial markets is struck closer to the price of the “underlying” than ever before, and doubt that limitless liquidity will trigger a dangerous rise in consumer prices. In all fairness, this glass half full assessment is hardly a theoretical one, but one based on years of empirical evidence.

Normalize This!

The sell-side is at it again, publishing a one-year ahead “Adjusted” EPS figure for the S&P 500 that is unlikely to be achieved—and then affixing P/E multiples seen near an historic market peak to “capitalize” on those unlikely earnings.

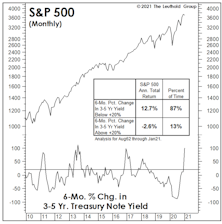

Minding The “Middle”

When investors ponder the level of yields that might pose a problem for stocks, it’s invariably the U.S. 10-Yr. Treasury bond that’s referenced. That’s fine, but the middle part of the Treasury curve has had just as strong a relationship with stocks, historically, as have longer-dated bonds.

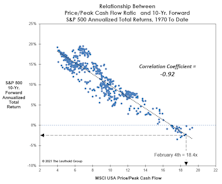

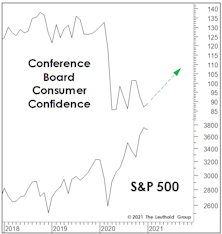

Climbing The Wall Of Confidence?

Stock market valuations may be considered the ultimate in fundamental measures, but they can just as easily be considered long-wave sentiment indicators. What causes equity investors to pay as little as 10x for S&P 500 Normalized Earnings at one point (March 2009), but pay more than 30x a dozen years later? The Fed printing press was in overdrive at both points; only emotions can account for the difference.

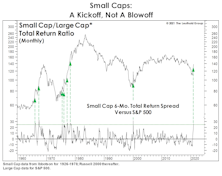

When “Overbought” Is Bullish

The recent months’ surge in Small Caps has been historic, and the Russell 2000 continues to register ridiculously “overbought” readings on many technical oscillators. In the short-term, that might be a cause for caution on the overall market. However (and perhaps counter-intuitively), this extreme strength cements our view that a long-term leadership cycle in Small Caps is underway.

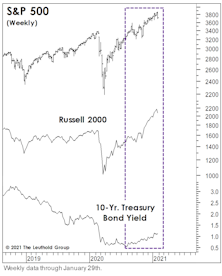

Stocks In The Face Of Rising Yields

With yields on the 10-Yr. Treasury finally breaking above 1.00% last month, the consensus has quickly evolved to the view that stocks and yields can continue to rise alongside one another for a while. Small Caps have shown a decisive performance edge during the recent episodes.

A Sign It Could Get “Even Sillier”

The January moves in heavily shorted Micro Caps were more bizarre than anything we saw during the wildest days of the Tech bubble. Despite these signs of rampant stock speculation by the retail crowd, we still wouldn’t characterize today’s sentiment backdrop as frenzied as the peak levels of 1999-2000.

How It Bodes For Biden

Early evidence suggests the Biden administration and the newly “purple” Senate will resist the pull of the far-left, at least from an economic perspective. Stock investors are cheering... though in light of their current euphoria, they might as well have celebrated a write-in victory for Ralph Nader alongside Green Party control of the Senate.

Putting Two Market Maxims To The Test

For decades, stock market observers have viewed January’s action as a harbinger for the rest of the year. Is there any merit to that belief?

Energy: A Curse And A Blessing

The Energy sector emerged as the top performer for January, a nice respite after a terrible 2020—but not exactly a good omen. Unlike in horse racing—where the concept of “early speed” has significant predictive power—the early leader in the sector-performance sweepstakes hasn’t reliably followed through in the last 30 years.

Passive’s “Placid Pandemic Performance”

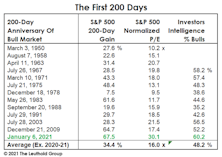

The 200-day “report card” for this bull market shows the best initial-performance gain of all postwar bulls, but it’s come at a price. Investor sentiment is above levels seen at the same point of past bull markets… and there are the valuations.

What If It’s Just A “Median” Bull?

Last spring and summer, we were incorrectly skeptical that a new bull had been born only five weeks after the death of oldest bull ever. But be careful with labels. Just as the “bear market” mindset caused us to overplay our hand last spring, equity bulls should not assume the current bull will look anything like the decade-long affairs we’ve seen twice in the last 30 years.

Y2K 2.0?

Cap-weighted valuations for the S&P 500 and S&P Industrials are homing in on the all-time records seen in the first quarter of 2000. We’ll confess that after those valuations collapsed in the years that followed, we thought we’d never see them again in our lifetime—let alone a mere generation later.

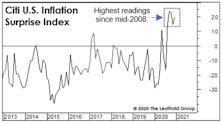

Heating Up Quickly

Inflation surprises have run hotter in the U.S. than in the rest of the world, no doubt reflecting the strength of major currencies versus the U.S. dollar.

Triggered!?

In recent months, we’ve highlighted some reasons to buy or add to Emerging Market equities, and at year-end received a formal endorsement from our monthly Emerging Market Allocation Model. The signal triggered after a 30-month period in which the model recommended the relative “safety” of the S&P 500—in retrospect, a good call.

The Case For “Five Percent”

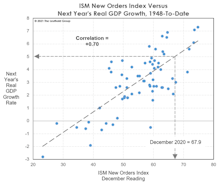

Forecasting GDP is hardly our forte, but 2021 should see a very big gain in real output. Our current guess is for real GDP to grow 5% this year. Statistically, though, that doesn’t imply that the stock market’s move will also be large (or even of the same “sign”).

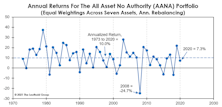

Liquidity Didn’t Lift Quite Everything In 2020

Last year should have been a perfect one for “diversification” to shine. Extremely high equity valuations entering 2020? Check. A recession-induced bear market? Check. Massive monetary and fiscal stimulus designed to lift all boats? Check and check.