Inside The Stock Market ...trends, cross-currents, and outlook

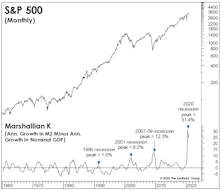

Liquidity: As Good As It Gets?

Stock market manias thrive on buzzwords, and if there’s a single one that captured the essence of the late 1990s’ boom it was “productivity.” In today’s version, our top candidate is “liquidity”—and we doubt anyone would argue.

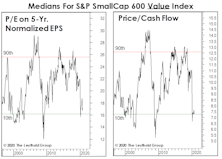

Small Value Or Small Growth? Yes!

If there’s an emerging bubble in Growth stock investing, it certainly doesn’t apply to Small Caps. The “usual” premium for Growth over Value within the Small Cap space is nonexistent—both segments look historically cheap.

VLT’s Struggles Are Telling Us Something

Our Very Long Term (VLT) Momentum algorithm has been a very good “confirmatory” market tool over the years, especially at the onset of a new cyclical bull market. But VLT has proven to be of little to no value in navigating this year’s gyrations. VLT’s latest flip-flops reinforce our view that the market leaderboard is set to be rearranged.

Tough Times For Allocators

Diversified, multi-asset portfolios have been weak performers for many years. The ultra-flexible, macro hedge-fund manager represents one extreme of the asset allocation continuum. At the other extreme would be the passive holder of multiple asset classes. It’s been a tough three years for this breed, too.

Time For EM Stocks?

On the basis of both Normalized P/E and Price/Book, there’s plenty of runway for EM stocks if they get back to even the midpoint of their 20-year valuation range. Rising commodity prices and a weak dollar would obviously help, and we expect both in the year ahead.

Miscellaneous Musings On Inflation

We’re still coming to grips with Modern Monetary Theory and the stark realization that “the delusional is no longer marginal.”

Energy: Still Too Early

Fundamentally, we don’t have much new to say on the disaster that Energy-sector equities have become. Mostly, we want to illustrate the danger of assuming that the stocks of commodity producers will necessarily follow the path of their underlying commodities.

SPACs: More Analysis Of Past Deals

Last month, we briefly discussed a burgeoning investment vehicle—Special Purpose Acquisition Companies (SPACs), also known as “blank-check companies.” Since the sole purpose of a blank-check company is to find an operating business to merge with, and subsequently bring it public, the best method to gain some understanding about the outcome of these relationships is to look at past deals.

The New FOMO

“Bull markets climb a wall of worry,” the old saying goes. We’ve heard that piece of wisdom (or imagined we heard it) every week since early summer. But we doubt it was meant to apply to today, when the paralyzing fear is not of potential loss, but of foregone upside (i.e., fear of missing out, or FOMO).

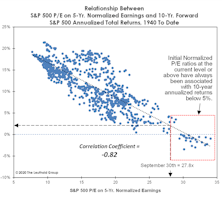

A Fast Start Comes At A Big Price

The first up-leg of the bull market has catapulted many Large Cap valuations to levels seen only in 1999, 2000, 2019, and pre-pandemic 2020. At the six-month point on September 23rd, the S&P 500 P/E on 5-Yr. Normalized EPS had already reached 26.9x—a reading that is 30% higher than at the same point of any other bull market.

Inflation In The Wrong Places?

Long before policymakers’ extreme response to the COVID collapse, we feared that the Fed’s interventions were suppressing important signals from the stock and bond markets. But we now suspect that hyper-expansionary policies are suppressing price signals from the “real” economy as well.

The Valuation Case For “SMIDs”

Mid and Small Cap stocks underperformed in 2018 and 2019. However, after the collapse of February and March, these “SMID” Caps have largely kept pace with the torrid rebound in the blue chips. Today’s valuations are priming the SMIDs for a similar “decoupling” in the years ahead, like that following Y2K.

The Use And Abuse Of Corporate Debt

U.S. corporations piled on almost $1 trillion in debt over the first six months of the year (a 10% increase). Corporate debt has now surged to 56% of GDP. We’ve argued that the level of corporate debt isn’t the problem, in and of itself. Rather, it’s what this debt has failed to generate that is the real problem.

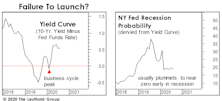

Remember The Yield Curve?

It would be a mistake to ignore (as most pundits will) this important forecasting tool until the next time it threatens to invert. The level and direction of the yield curve provide helpful information throughout the entire economic cycle.

Tech Mania 2.0 Doesn’t Quite Measure Up

In the 24 months leading up to its early-September peak, the S&P 500 Technology sector gained 68%. By comparison, the two-year S&P 500 Technology gain going into its March-2000 peak was 203%. The S&P SmallCap 600 Technology Index doubled in the 23 months leading into the early-2000 top versus the two-year gain of just 6% at its 2020-summer peak.

Homebuilders: The Weird And Unexpected

Like many years, 2020 is one in which an investor who was armed with a perfect economic forecast would have been befuddled by stock market action. Who would have imagined that passive equity investors (including many posing as Wall Street strategists) would be so well-rewarded for ignoring the economic downturn?

Five Reasons To Expect Higher Yields

Much of what we think “we know” about the bond market says yields should be headed higher.

SPACs: Fashion Or Fad?

Special Purpose Acquisition Companies (SPACs) have become increasingly popular of late. We ask a seemingly simple question: “How do companies fare following a SPAC merger?”

Musings On A Manic Market

Officially, those quick to pronounce the move off March lows as a new bull market have been proven correct with new S&P 500 all-time highs. Fundamentally, though, there’s enormous risk in Large Cap valuations, regardless of where one believes we are in the economic cycle.