Chart Of The Week

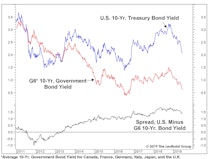

Limbo Rock!

As global rates have taken a precipitous dive the last few months, it’s been hard not to hum “Limbo Rock.” And just like Chubby Checker, we’ve been asking our screens “How low can you go?” on a daily basis.

The Market Is On Fire… Unless It’s Ice

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Yesterday’s S&P 500 new all-time high triggered a few simple internal studies we’ve used to help shape second-half expectations for the stock market.

Deflation And Deception

.jpg?fit=fillmax&w=222&bg=FFFFFF)

We think the current economic cycle is more likely to end in a deflationary bust than with a bout of late-cycle “overheating,” and analysts and investors should recognize that such a cycle ending could be especially difficult to detect.

An Economy This Healthy Is Hostile To Profits

.jpg?fit=fillmax&w=222&bg=FFFFFF)

It’s hard to grow profits when an economy’s resources are already fully employed, a fact we highlighted when the U.S. Output Gap turned positive several quarters ago. Therefore, the first quarter drop in NIPA corporate profits, reported yesterday, shouldn’t have come as a surprise.

First Quarter Earnings Waterfall

What a difference a year makes! In early 2018 we were celebrating 20% earnings growth, driven by a strong economy and the massive corporate tax cut. Sales were rising at a double-digit rate and the tax burden was shrinking dramatically, setting up one of the best earnings years in history.

Microsoft Reclaims The Iron Throne

Even our staid and august firm isn’t above a little Game of Thrones clickbait.

After nineteen years in the wilderness, an old king has returned for his throne. The House of Microsoft is once again the most valuable company in the S&P 500 and, as of last month, is the sole occupier of the “4% Club” (i.e., weighting in the index).

Non-Energy Commodities Signal A Major Slowdown

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Late in the cycle, blue chip indexes like the DJIA and S&P 500 can fool investors by hiding subtler deterioration in the broad list of stocks. That’s been underway in the last couple of months, but it’s nothing in relation to the divergence that’s opened in the commodity market, where there’s an almost 20% YTD performance gap between the headline S&P/GS Commodity Index and its non-Energy components (Chart 1).

Adding Some Emerging Markets On A “Rent-to-Own” Basis

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Emerging Market equities have been modest underperformers during the current rally, but they’ve marshaled enough strength to trigger a new low-risk BUY signal on our VLT Momentum algorithm at the end of April.

Oil And The Dollar At New Highs: Is Something About To Give?

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Crude oil and the U.S. Dollar Index accomplished a relatively rare feat by moving to simultaneous six-month highs earlier this week (Chart 1).

Small Caps And The Recent “Rate Hike”

The 1999 leadership parallels we discussed in the latest Green Book remain intact—U.S. over foreign, Growth over Value, and Large over Small. Small Caps have given up most of the “beta bounce” enjoyed in the first two months off the December low, with one Small Cap measure—the Russell Microcap Index (the bottom 1000 of the Russell 2000)—undercutting last year’s relative strength low and those of 2011 and 2016.

Margins Prove Capitalism Still Works

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Corporate profits were outstanding last year, but even the benefit of a 40% cut in the top income-tax rate wasn’t enough to lift the net profit margin back to the all-time high of 10.6% established in early 2012. Still, the latest 10.0% figure is more than a percentage point above the 2007 cycle high and about two points better than any other cycle high.

The Cycle Is Over If Confidence Fades Further

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The “Expectations” component of the Consumer Confidence survey has been wobbly in the last few months, but the latest report, released on Tuesday, showed the first meaningful hit to consumers’ “Present Situation” since the stock market first began to struggle 14 months ago (Chart 1).

Partying Like It’s 1998-99

.jpg?fit=fillmax&w=222&bg=FFFFFF)

We thought Jerome Powell’s “Christmas Capitulation” would be tough to beat, but he accomplished that two days ago with what could be called his “Spring Surrender.” That, in turn, has rekindled hopes of a stock market melt-up along the lines of 1998-99, which, as old-timers will remember, followed a late-cycle correction that was nearly identical to the one seen last year.

Be Wary Of The “E” In P/E

.jpg?fit=fillmax&w=222&bg=FFFFFF)

U.S. equity valuations remain considerably higher than those of any major foreign market, but there’s no denying they’ve improved from the cyclical peak made in January 2018. That’s true across the capitalization spectrum, and on the basis of both normalized and non-normalized fundamentals.

So Long Tax Cuts… We Hardly Knew Ye

Our earnings waterfall analysis for the fourth quarter tells a story consistent with the entirety of 2018: earnings growth was fantastic, boosted by the twin drivers of strong sales growth and a lower corporate tax rate. Chart 1 spotlights the quarter’s tally, which produced a healthy sales growth number despite some economic weakening.

Assessing The Cyclical Risks

With all the excitement over the Fed’s shift in rhetoric and the excellent subsequent market action, there’s a danger of losing sight of the broader cyclical backdrop for U.S. stocks. Remember, the economy is still operating beyond government estimates of its full-employment potential, and it’s not as if the Fed has actually eased policy—as it did successfully at a similar late-cycle juncture in the fall of 1998 and (ultimately unsuccessfully) in the summer of 2007.

Momentum Buyers: Beware

Momentum is a smart beta factor that gives investors excellent upside participation in rising markets. Most other smart beta factors are defensive plays, so Momentum is the place to be in strong upward moves. Momentum filled that role admirably in recent years, rising 56% from 2016 to the September top, compared to an average of +26% for the other major factors.

2019 Earnings: Don't Bet On 6%

Currently, the collective intelligence of Wall Street is predicting 6% S&P 500 EPS growth in 2019. It’s also the 61-year average annual growth rate for the index, so how wrong could it be?

John Bogle: Investment Philosopher

The passing of investment legend John Bogle has brought forth many well-deserved tributes to his professional accomplishments. He was a tireless champion of passive investing and the founder of The Vanguard Group which, as more than a few investors don’t realize, also manages almost $1 trillion in active funds.

The Trump Trade, Two Years In

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Donald Trump is thought to have been born with a silver spoon in his mouth, and the economic circumstances prevailing at his inauguration two years ago might have further perpetuated that view. The U.S. economy had already been in recovery mode for 7 1/2 years, and the bull market in U.S. stocks was about to celebrate its eighth birthday.