Chart Of The Week

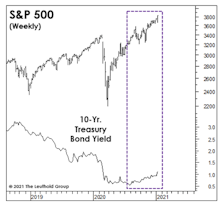

Stocks And Yields Revisited

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The S&P 500 and 10-Year Treasury bond yield could accomplish something fairly rare today by closing at “joint” 52-week highs. The relevant levels to meet or exceed are 3934.83 on the S&P 500 and 1.49% on the bond yield.

Carbuncles, Diamonds, and Tears

.jpg?fit=fillmax&w=222&bg=FFFFFF)

High growth rates, innovation, and disruption are defining traits of the companies that have powered the market to recent highs, and the ARK Innovators Fund (ARKK) is an example of today’s enthusiasm for visionary growth stocks. Recent returns and growth in AUM have been nothing short of spectacular, and ARKK has become symbolic of today’s style of new-era growth investing.

Has Liquidity Peaked?

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The last few weeks offer plenty of evidence that the mania has moved into a more feverish phase, yet the Fed insists that it is still “not-even-thinking-about ‘thinking about’” raising interest rates. That dismissive attitude could well whip up an even higher fever in the months ahead.

An Historical Look At Biden’s “Future”

.jpg?fit=fillmax&w=222&bg=FFFFFF)

We’ve read far too much about what Joe Biden and a newly-blue Congress might do in the months ahead, but less so about the conditions Biden and his team inherit. Such “initial conditions” usually have a heavy hand in policy outcomes, market outcomes, and even a president’s legacy.

Inaugurations And The Stock Market

Presidents and the popular press have become obsessed with performance over the “first 100 days” in office. That prompted us to see if there have been any persistent stock market effects related to this 100-day window. There are many ways to slice the data, and the more we sliced it, the fewer the observations.

Rising Rates And Rising Stock Prices?

Often, what market pundits like to pass off as bold, contrarian forecasts are merely rationalizations and extrapolations of trends that have already been in place for some time.

Looking Forward To 2021 Earnings

.jpg?fit=fillmax&w=222&bg=FFFFFF)

As we turn the page on 2020, a peek ahead to the S&P 500’s 2021 operating earnings is probably in order. You never know, earnings and valuations might be important again one day.

The “Pfizer Factor Flip” And Fund Flows

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Pfizer’s November 9th announcement of an effective COVID-19 vaccine triggered the most extensive one-day rotation in style factors we have ever seen. Investors flipped from Large Growth—the market’s dominating style over the past few years—and found new friends in Value and Small Cap. This rotation continued through November, to the point that Value and Small Cap each had their best single-month return in 30 years.

Bond Yields: Cyclical Pressures Vs. Positioning

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Even after watershed events COVID-19 and MMT, some things never change.

Next year will begin like almost every one of the past dozen years, with economists and strategists expecting bond yields to rise.

Unlike most of those years, though, there are several measures of “cyclical pressures” that would seem to give them a good chance of being right. The best-known among these might be the “Copper/Gold Ratio,” popularized by DoubleLine’s Jeffrey Gundlach, which suggests 10-Yr. Treasury yields should be around double their current level (Chart 1).

The “Transportation” Divergence

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The Dow Jones Transportation Average has recently notched fresh all-time highs. Following a sizable relative performance dip earlier in the year, the Transports’ relative strength has recovered and moved to new 2020 highs (Chart 1). Still, compared to the broad market, the index’s YTD return appears fairly unremarkable, outpacing the S&P 500 by about 3%.

The Rotation Should Hardly Be A “Surprise”

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Consumer Price Inflation of 1.2% for the twelve months through October remains way below the Fed’s long-time 2% objective, which is nothing new. But a first step in getting inflation to eventually run a little bit “hot” (the Fed’s new objective) is to break the long-term disinflationary psychology among consumers and investors, and that is clearly happening. In fact, based on the excellent “Inflation Surprise” Indexes published monthly by Citi, the U.S. is now the world’s inflationary hotspot!

Momentum’s Terrible, Horrible, No Good, Very Bad Day!

.jpg?fit=fillmax&w=222&bg=FFFFFF)

If Momentum and Growth investors thought they were escaping 2020 unscathed, they learned otherwise on Monday. Pfizer’s promising news about a COVID-19 vaccine was met with universal excitement and investors rearranging portfolios—taking gains in long-term winners and plowing into beaten-down cyclical stocks.

It’s Time To Choose

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Which box do you check? The “status quo” or the “change of pace?” Keep in mind, the same decision in front of you turned out to be extraordinarily important four years ago. So, which will it be for 2020 and beyond? Large Cap Growth or Small Cap Value?

Election—Another Chance For Value

.jpg?fit=fillmax&w=222&bg=FFFFFF)

As we Chinese watch the elegant display of the western democratic process this election season, we can’t help but think there are indeed people less fortunate than us “commies.” Worse yet, some of these people are Value investors.

Leuthold Factor Tilt Update

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Factor analysis is a point of emphasis in Leuthold’s tactical research activities, and this note summarizes our Factor Tilt outlook going into the fourth quarter. Factors are return drivers such as Value, Momentum, and Quality, and research has found that factor results vary over time—but that does not mean they are random.

Small Cap Catch-Up?

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The big jump in Small Caps over the last two weeks has entirely reversed the segment’s summer underperformance and has technicians feverish about another “breath thrust.” Technically, it’s impressive, but we are more intrigued by the fundamental potential for continued Small Cap (and Mid Cap) outperformance.

European Banks: Buy Low…?

.jpg?fit=fillmax&w=222&bg=FFFFFF)

As steadfast believers that “price paid” is a major determinant of an investment’s risk and return, we snap to attention whenever we hear that an asset is selling at a multi-decade low.

A Wobble At The Top

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Look, quick! Before it reverses! The Top-5 firms in the S&P 500 have underperformed in September! I’m sorry, you’ll have to forgive my sense of urgency, but the astounding speed and consistency in which these firms have outperformed may have burned the notion into my brain that they can only “go up” (or at the very least beat the index).

Inflation: Looking Beyond The CPI

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The Fed is hell-bent on generating inflation of 2% or higher in an over-supplied world that we think should probably be experiencing mild deflation. Their success or failure at this mission will be critical for asset allocators. For equity managers who must remain fully invested, however, the more important question might be not whether the Fed can generate higher inflation, but where.

“Guess What’s Been Exceptional?”

.jpg?fit=fillmax&w=222&bg=FFFFFF)

How can an equity manager possibly keep up with the QQQ—an ETF that’s almost 50% invested in the six largest U.S. companies?

Easy! Own the vehicle that benefits the most from a collapse in global trade volume and an escalating cold war between the U.S. and China—the EEM (iShares MSCI Emerging Markets ETF)!