Inside The Stock Market ...trends, cross-currents, and outlook

High Quality Stocks Rally Back

Stocks with High Quality rankings have outperformed those with Low Quality rankings for the past few months. The junk rally is at or near an end, and investors may want to shift their attention to High Quality stocks.

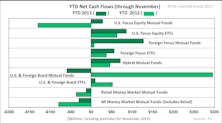

2013’s Fund Flow Trends Have Room To Run

Year-to-date, equity funds are cash on par with those of the 2000 tech bubble, while bond mutual funds are experiencing net cash outflows for the first time in a decade.

Implications Of Increased Access To Chinese A-Shares

There are signs the domestic Chinese market may be more accessible to global investors sooner than most think. We explore the implications of these potential changes.

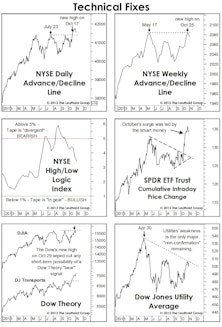

No “Pop,” Just A “Hiss”…

In the 1970s, a cassette tape manufacturer asked listeners, “Is it live, or is it Memorex?” Forty years later, watchers of the stock market “tape” find themselves asking, “Is it real, or is it QE?”

Little To Complain About

From a pure price action perspective, it’s difficult to find cracks in the bull market’s edifice.

Stock Values: Absolutely, Relatively

The severity of the market’s current overvaluation depends on one’s historical vantage point.

Beyond P/E Ratios

Some of our alternative valuation measures find the market even pricier than P/E ratios do.

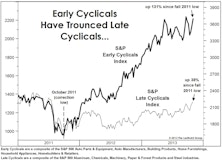

Cyclical Stocks: Is It Finally Getting “Late?”

There’s no reason to run for cover if the Early Cyclicals have topped out.

Introducing A New Regional Equity Model…

That leads us to think more about price momentum as an alpha-generating factor.

Is Low Volatility A Warning?

Low volatility isn’t a bearish omen in and of itself, and we found stock market volatility levels to provide much near-term directional help.

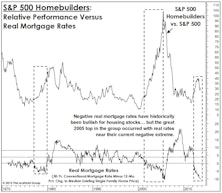

Housing: Just Like The Bubbles Before It

Sectors that become the object of obsession during one economic cycle tend to remain cyclically depressed in the following one.

Global Valuations Rising, But U.S. Still At A Premium

The large valuation discount on foreign shares has narrowed a bit, reflecting better relative action in foreign shares over the past 14 months and relatively weaker foreign fundamentals.

Valuations & Future Returns

The U.S. market rates anywhere from mildly overvalued to very overvalued relative to other developed markets. Foreign markets might be the last remaining pocket of yield that isn’t overvalued.

The MTI, And More Market Maxims...

Someday in the faraway future, in the midst of a low-volatility, peace-time bull market, we plan to write a Green Book “Of Special Interest” piece on the investment wisdom of Yogi Berra. “Ninety percent of the game is half mental.” Classic. “You can observe a lot by watching.” Words that I live by.

Market Internals: The Good And The Bad

Leadership isn’t warning of impending weakness in either the U.S. economy or the stock market. Market breadth, on the other hand, is highlighting risks that aren’t evident when inspecting leadership alone.

Is The Dividend Mania Ending?

The list of new lows is dominated by yesterday’s darlings, “bond-like” stocks. In particular, Utilities and REITs have been hammered. However, not all of the stock market’s high yielders have been trashed.

Small Cap Cycle Extension?

Small Caps have an historically high P/E premium of 15% vs. Large Caps. This premium could go higher, but we’d be reckless to call for a long-term extension of Small Cap leadership given this premium.

Industry Groups: No Need To Bottom-Fish

Buying global groups with strong price momentum has been a winning strategy. Will it continue?

Decomposing Today’s Record Profit Margins

The celebrated gains in corporate profitability over the past decade and a half are attributable primarily to proportional declines in “below the line” items like interest expense and corporate taxes.