Macro Monitor

Textual Analysis Of Fed Statements—Always Artificial, Sometimes Intelligent

We geek it up a notch and use some of the popular text-processing techniques to quantify the hawkish/dovish sentiment of the latest Fed statement. Some human “coaching” is needed in every step of the process (hence the “artificial” part). But when these tools are used properly for carefully chosen tasks, they can be quite intelligent.

Risk Aversion Index: Stayed On “Lower Risk” Signal

With “reopening” taking a pause, we expect global policies to remain accommodative even longer. Among fixed income, we like corporate credit, which includes both investment grade and high yield bonds.

No Yield Curve Control? The Fed Spoke Too Soon

There has been chatter about the Fed implementing the so-called Yield Curve Control (YCC). Although the latest FOMC minutes suggest that YCC is not on the agenda for now, we believe the chance of YCC is probably much higher than the market currently anticipates.

Risk Aversion Index: Stayed On “Lower Risk” Signal

While the market seems to have priced in a quick recovery, recent economic data has materially exceeded market expectations and provided support to the rally. Within fixed income, we maintain a favorable view toward investment-grade corporate bonds and we still recommend staying within range of the Fed’s fire power.

The State Of The Stock/Bond Relationship

The latest action in rates is not what would be expected during a strong stock-market rally off a bear market low, but the constantly changing nature of the stock/bond relationship should not come as a big surprise. We propose a more refined four-state definition of the stock/bond relationship.

Risk Aversion Index: New “Lower Risk” Signal

Our Risk Aversion Index fell sharply in May and generated a new “Lower Risk” signal. Within fixed income, we are turning more constructive on credit, overall, and maintain our favorable view toward investment-grade corporate bonds.

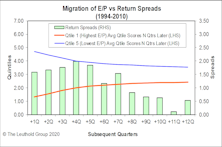

Why Value Failed—Top-Down & Bottom-Up Views

From a top-down view, since 2003, Value’s performance has been much more closely tied to various asset markets and macro drivers. From a bottom-up perspective, we believe the change in Value’s migration behavior might be the key to its failure. We believe macro tailwinds and positive surprises are both necessary for a true Value revival.

Risk Aversion Index: Stayed On “Higher Risk” Signal

While macro data has turned from “bad” to “less bad,” a lot of hope for a quick recovery in economic activity has been priced in. We recommend staying within range of the Fed’s fire power for the time being.

A Cross-Asset Dash For Cash

March’s mad dash for cash didn’t stop with rates/credit/FX markets. Among equities, there was also a strong preference for cash liquidity. The market rewarded companies that had strong cash positions and punished those without—which explains why traditionally defensive styles actually underperformed.

Double-Digit Yield & Double-Dipping Curves

As the coronavirus materially increases the odds of a recession, some important parts of the U.S. yield curve (10Y-3M; 5Y-2Y) double-dipped into inversion. The two prior episodes occurred in late 1989 and mid-2006 and, in both cases, a recession followed within 18 months.

Risk Aversion Index: Stayed On “Higher Risk” Signal

We will remain cautious toward lower-grade credit until we see the peak in new coronavirus cases. It all comes down to the recession call and the coronavirus has significantly increased recession risk.

Coronavirus—An Accelerator, Not A Catalyst

Chinese and Hong Kong markets are currently following the same script as seen during the SARS outbreak, but we caution against using S&P 500 performance as a guide for what is likely to happen this time around.

Risk Aversion Index: New “Higher Risk” Signal

We are turning more cautious toward lower-grade credit and will likely remain so until we see the peak in new coronavirus cases.

The Decade Of U.S. Exceptionalism & The Year Ahead

Two words sum up the past decade pretty nicely: U.S. Exceptionalism. The superiority of U.S. assets really comes down to the unique combination of growth (U.S. stocks), yield (U.S. bonds), and relative safety (both U.S. stocks and bonds).

Risk Aversion Index: Stayed On “Lower Risk” Signal

While the overall near-term tone is still positive for risky assets, complacency seems widespread too. This tempers our enthusiasm to chase risky assets at this point.

Slowdown Or Recession? No Confidence In “Confidence”

The ultimate question is whether the Fed’s recent “insurance cuts” are enough to overcome uncertainties about trade talk—and the upcoming election—to avert a recession. We updated our “Slowdown vs. Recession” study to see where we stand now. The bottom line is: It’s too early to rule out a recession.

Playing With Fire & Ice—An Inflation Scorecard

We put together an Inflation Scorecard that monitors two critical sets of inflation drivers: demand pull and cost push. The qualitatively-adjusted score is much closer to a neutral reading than the mechanical composite (which suggested quite a bit more disinflationary headwind).

Risk Aversion Index: New “Lower Risk” Signal

We are turning favorable again toward credit, especially emerging market sovereign debt.

Cross-Asset Cross Currents—All About The Recession Call

September was an emotionally exhausting month for investors as reversals in major themes produced wide-ranging repercussions. Movements in various markets have been increasingly tied to bonds—the market that is most sensitive to recession outlook.

Risk Aversion Index: Fell But Stayed On “Higher Risk” Signal

Recent data has certainly increased the risk of an imminent recession, but more confirmation is needed to move us into the recession camp.