Macro Monitor

Risk Aversion Index—Ticked Up But Stayed On “Lower Risk” Signal

The real test for risky assets lies immediately ahead with central bank meetings, the Brexit vote, and the Spanish election later in the month. We continue to favor Higher Quality credits within fixed income.

Reflation Trade Back In Vogue? We’d Rather Be Late Than Early

Despite recent improvement in some inflation measures, we are not convinced the war against disinflation has been won. The risk of being too early on the inflation call far outweighs the risk of being too late.

Risk Aversion Index—Stayed On “Lower Risk” Signal

After the last couple months’ strong surge, risky assets are entering a seasonally unfavorable period, with Brexit looming particularly large in the near term. We still favor higher quality credits within fixed income.

The Fed’s Capitulation To The Dovish Side— A Win-Win For EM & U.S.

We have mentioned a number of times that China had experienced a very unpleasant “second-hand” tightening due to its peg to the dollar. Its trade competitiveness has suffered tremendously. With a weaker dollar the Chinese Yuan can re-gain some of its competitiveness while maintaining its peg to the dollar. A rare win-win in today’s convoluted world of finance.

Risk Aversion Index—A New “Lower Risk” Signal

We are getting more constructive on credits but we are still keenly aware of the highly volatile market environment and would recommend modest exposure to lower quality credits at this point.

U.S. Investment Grade Corporate Bonds: Maintain Favorable

More spread compression is likely ahead.

U.S. Municipal Bonds: Maintain Unfavorable

There is still a lot more room for Munis to underperform Corporate bonds.

U.S. High Yield Corporate Bonds: Maintain Neutral

We will be looking for a good follow-through to consider an upgrade of these bonds.

Risk Aversion Index—Ticked Lower But Stayed On “Higher Risk” Signal

We believe a short term rally is more likely and recommend a neutral stance towards credits at this point.

New Bond Market Record: G5 10-Year Average Hit All-Time Low

Despite the improvement in market sentiment, U.S. bond yields were dragged lower by their international counterparts.

Muddle-Through Still Has The Benefit Of The Doubt

The market’s latest infatuation with bonds was driven by grave concerns that the weakness in energy and manufacturing sectors might be spreading to the U.S. economy as a whole.

Market’s Message To The Fed: Stop The Tightening!

We think the Fed’s projection of four more hikes this year is absolutely unachievable, and we are no doubt siding with the market’s current projection of one hike, at most (if any), this year.

The Current State Of Stock-Bond Relationship: Risk-Off

The transition we saw last year from a mostly Risk-On (or Easing) environment to a more challenging Tightening (or Risk-Off) environment has made the relationship especially volatile.

Risk Aversion Index—Moved Up; A New “Higher Risk” Signal

We are aware of the oversold condition in oil but we expect volatility to remain high in the near term. We maintain a defensive stance towards credits at this point.

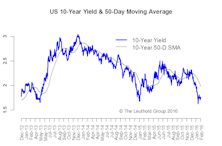

2015 - All Risk And No Reward

The U.S. 10-year yield was quite volatile, fluctuating in a 100 bps range between 160 and 260, and ending up a mere 10 bps higher for the year. But it was still better than most other major asset classes which saw all risk and no reward.

2016 Time Cycle—Not Likely To Be A Typical Year

The 2016 pattern looks good on paper, but if the excitement in the first week of the year is any indication, we highly doubt 2016 will turn out to be another typical election year.