Inside The Stock Market ...trends, cross-currents, and outlook

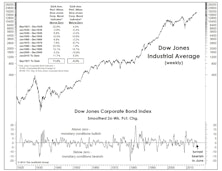

A Venerable Monetary Indicator Turned Negative

The smoothed, 26-week rate-of-change in the DJ Corporate Bond Index, a reliable indicator of monetary conditions over many different market and economic cycles, turned negative in mid-June.

Leadership: Winning Begets Winning

Many assume that stocks and industries exhibiting high price momentum suffer disproportionately during the eventual bear market. Surprisingly, the high momentum stock portfolio has suffered an average bear market loss that’s about a quarter less than that of the low momentum portfolio.

Oil Prices And VLT

Energy groups continue to rate poorly in our quantitative work, but change will probably be afoot in the second half.

What’s Next For The Dollar?

The U.S. Dollar Index has recovered about half the losses from a two-month, -7% setback from the 12-year peak it established in March.

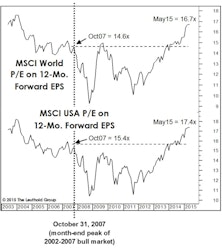

A Kind Word For “Forward Earnings”

Our criticism of the widespread trust in “forward earnings” has sometimes been harsh, but consider the following: the latest 12-month forward EPS estimate for the EAFE index is $122.71, virtually matching the forward estimate that was made in January 2006.

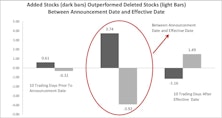

“Index Rebalance Effect” On Stock Performance

Stocks selected for inclusion in the MSCI ACWI have outperformed from the day of the announcement to the day of implementation, while the opposite is true for stocks which are removed. Long-term, however, stocks included in the index do not outperform compared to those that were removed.

High Quality Outperforming, But Valuations A Concern

High Quality stocks had another winning quarter on a relative basis returning +0.1% in Q2, while Low Quality stocks lost 2.8%. Small Cap High Quality stocks also beat their counterparts.

Don’t Fight The Fed?

While our stock market disciplines (including the Major Trend Index) are nominally bullish, we’re mentally gearing up to do something in the near future that was once considered ill-advised: Fighting the Fed.

Another Retrospective On The Bull…

Up front, we need to remind readers that the Major Trend Index is bullish at 1.08, and our tactical funds remain well-exposed to equities with net exposure of 60-61% (versus a range of between 30% minimum up to a maximum of 70%). That being said, we’re focused on the likelihood of a major defensive portfolio move in the near future, which probably comes as no surprise to Green Book readers (...what with us publishing a prepackaged obituary for the bull market just a month ago).

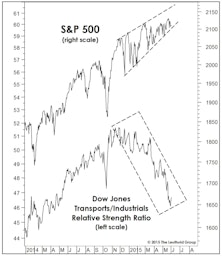

Transports Still Troubling

The Dow Jones Transports lagged the market badly again in May, and continues to stand tallest among the red flags we’re now monitoring.

The Double Death Cross!

The Dow Transports and Dow Utilities both triggered major sell signals in May when their 50-day moving averages fell below their 200-day moving averages… known by some as a “Death Cross.”

Two Takes On Market Breadth

Market technicians continue to argue that a bull market peak is unlikely to form with the majority of U.S. stocks (and global ones, for that matter) still participating in the new highs of the blue chip indexes.

Stock Market Valuation Check

It now goes almost without saying that whenever the stock market moves to a new cycle extreme, so does the MTI’s Intrinsic Value category. In late May, this reading dropped below –400 for the first time in this bull market, and is now within 150 points of its 2007 extreme.

Yet Another All-Time High...

It’s generally a bad idea to roll out new valuation readings that one doesn’t fully understand late in a cyclical bull market. But we’re going to do it anyway, recognizing that a similar practice proved to be the undoing of dozens of fund managers and Tech analysts at the turn of the millennium.

What’s In Store For The Secular Bull?

Last year seemed to cement the view that stocks have entered a new secular bull market, and today we’re not going to offer our dissent—what with the S&P 500 trading about a third above its 2000 and 2007 “Twin Peaks”.

It’s Getting Late For the Early Cyclicals

Our “Early Cyclicals” composite continues to perform so well—and at such a late stage in the market cycle—that we should probably consider changing its name. This group, which consists of retail, housing, and auto-related industries, is up 29% in the last eight months after stalling out for the first three quarters of 2014. Its “Late Cyclical” counterpart is up just +5% over the same time frame.

Housing: Curb Your Enthusiasm

Despite record low mortgage rates and pressure to re-loosen down payment and lending requirements, single family housing starts have yet to recover to levels consistent with even the average recession trough.

Searching For Growth In Emerging Markets

Even though the ten EM sectors are growing at a much stronger pace than corresponding U.S. sectors on the Top-Line, only a small margin exceed the U.S. in terms of EPS growth.

Flying By Instruments

The safest highs to sell in the stock market are “lonely” new highs. Fortunately, the April 24th bull market high in the S&P 500 was anything but, as that index enjoyed a varied swath of Large Cap, Small Cap, and foreign company (although the DJIA was a mysterious no-show).