Inside The Stock Market ...trends, cross-currents, and outlook

Seasonality Of A Different Sort

In the June 2018 Green Book, we noted that stocks have shown a fairly reliable correlation with a calendar of an entirely different sort: the solunar calendar. It turns out that the days that our $9.95 “iSolunar” iPhone app predicts to be good ones for fishing (based entirely on phases of the moon) are the same days that stocks have enjoyed the largest average gains!

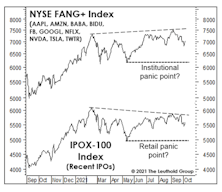

These “Insiders” Have Exited; Should You?

What if the S&P 500’s September 2nd closing high were to miraculously stand as the cycle’s high-water mark? If it did, the peak was presaged—in retrospect—by two Federal Reserve Bank presidents who rode the liquidity wave all the way to its crest after assuring the floodgates would be left wide open. Both resigned in September.

Deep Thoughts On The Recovery

Massive gains in stock market wealth have undoubtedly been a contributor to inflation, yet few analyses of the inflation picture even mention the stock market—other than to predict it will soar when inflation proves transitory.

The Trend Is A Bit Less Friendly

The MTI’s move to its Negative zone with the October 1st reading was driven by a few trend breakdowns—ones that could well reverse in short order. Recognizing the volatility of these signals (and perhaps having been “conditioned” by the one-way market of the last 18 months), we opted for just a minor asset allocation adjustment.

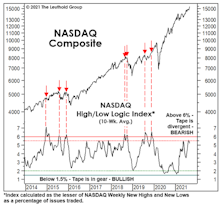

Yet Another Late-1990s’ Comparison

The post-COVID surge in the NASDAQ 100 has been a perfect match in terms of duration with the one following the crisis afflicting Russian debt (and the LTCM debacle) in the fall of 1998. Incredibly, both of these historic market moves lasted 369 trading—but that’s where the resemblance ends.

Are Price Hikes The “New” Rate Hikes?

Notwithstanding the hit to consumers’ pocketbooks, it’s been amusing to follow the Fed’s recent evolution with its mindset regarding inflation. A year ago, the hope was for “symmetry”—Fed-speak for allowing inflation to run above its long-time 2% target, since it had previously undercut that level for awhile. Then, early in 2021, the word “transitory” entered the lexicon; yet months of debate and tens of thousands of utterances on financial television have clarified nothing about the Fed’s characterization of that term.

Why Is Confidence “Inverted?”

In a recent “Chart of the Week,” we discussed the late-cycle “inversion” in Consumer Confidence, where consumers’ views of their “Present Situation” have jumped far above their “Expectations.” That’s the reverse of what’s typical in the first couple years of an economic expansion.

That Money Tsunami Is Now Just A Flood

Compare the U.S. monetary response in early 2020 to China’s: The Fed quadrupled the M2 growth rate (from 6% to 24%) in three months, while China merely bumped M2 growth from 8% to 11%. This relative policy restraint leaves China in a better position to handle potential fallout than if it had gone “all in” like the U.S.

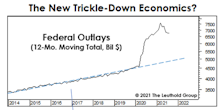

How It All Went “Down”

The COVID rescue plan has generated a multi-trillion-dollar deluge of federal spending that has trickled down to government transfer payments, personal incomes, retail sales, and surging EPS. When considering all of these data series in relation to their long-term trends, it’s truly remarkable that the only item analysts consider to be “transitory” is inflation.

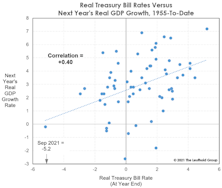

Rethinking Real Rates

Consumer Price Inflation has stabilized in the 5.2–5.4% range in the last two months, giving the Fed hope that it’s reached a near-term peak. Still, the presence of 5%-plus inflation in the face of ZIRP leaves the real short-term Treasury-bill rate about as deeply negative as it has ever been.

Valuations And The Earnings Recovery

Analysts at Standard & Poor’s will soon confirm what’s been known for several months: The earnings downturn associated with the COVID recession was the shallowest and shortest of any recession-related EPS decline.

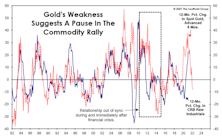

Gold: Still A Useful Dollar Hedge

A stronger U.S. dollar is “supposed” to be bearish for commodities, but it’s been a banner year for most commodities with gold among the few that are down on the year. However, keep in mind that gold tends to be a harbinger of major moves in industrial commodities, with a lead time of about six months—and its year-over-year change is now negative.

A Good Thing To Have In Reserve

It seems investors care mostly that the authorities have fiercely defended the S&P 500’s status as the World’s Reserve IndexTM. A decade of QE should have taught us that when the Fed conducts a decade’s worth of QE in little more than a year, U.S. Large Cap stocks benefit the most.

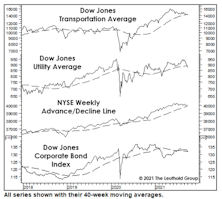

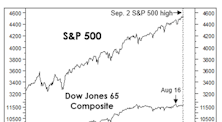

Reading The Short-Term Tea Leaves

The market’s August push was enough to lift four of the seven lagging bellwethers to new cycle highs. Among the three remaining laggards, only the Dow Jones Transports is still significantly below its high.

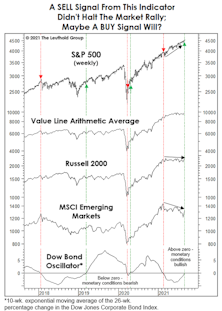

Let Us Add To The Bullish Cacophony

It’s been a heck of a stock market year, and there are still four months left. What else could go right? Monetary conditions, for one thing—at least as proxied by our Dow Bond Oscillator (DBO).

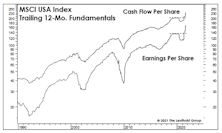

The Stock Market IS A “Fundamental”

The impact of U.S. stock-market “hegemony” extends far beyond currency markets. We believe the mania has progressed to the point where the stock market itself will shape the intermediate-term and even long-term fortunes of the U.S. economy more than it ever has before.

Technology Stocks: Dance Like Nobody’s Watching

In the middle of the last decade, we marveled at the Tech sector’s ability to flog the rest of the market quarter after quarter, with no meaningful breakout in valuations. Specifically, the median Price/Cash Flow ratio for S&P 500 Technology managed to “hug” the 15x level for about four years beginning in late 2013. Tech’s post-COVID boom is nothing of the sort.

What’s Your “Number?”

Those in their peak earning years (40s and 50s) who’ve also enjoyed the stock market’s windfall gains are very likely to have seen their annual expenses climb much higher than the Consumer Price Index over the last several years.

Not Overthinking Small Caps

There are some positive cyclical influences for Small Caps, like higher inflation and deeply negative real interest rates. But in our minds, the valuation spread versus Large Caps is more important.

A Lost Decade For Emerging Markets

Fading momentum in GDP growth, sizable dislocation of corporate EPS in the midst of an expansion, and U.S.-dollar weakness have all made EM equity investments inferior to U.S. stocks over the last decade.