Special Reports

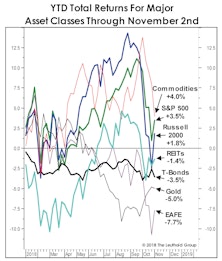

Asset Allocation: As Bad As It Gets

Asset Allocation in 2018 is about as bad as it gets. No major asset class has done well.

November 2018 Green Book Summary

We wrote in October’s Green Book that “many once reliable seasonal market patterns have been out of sync in recent years.” The market gods punished us for having the audacity to write such a thing (and during October, of all months!), taking the S&P 500 down to within 0.1% of “correction territory” at the October 29th low. But the punishment outside the U.S. commenced long beforehand, and last month’s losses drove several foreign market measures into bear territory. We expect U.S. blue chips to follow.

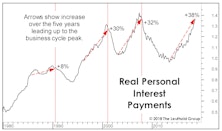

Rates Hurting Households

Doubling of yields since 2016 has slammed households. Percentage increase in rates is more important than the absolute level.

Factors And Sectors: A Curious Entanglement

Portfolio managers who tilt toward Value or Growth stocks have long known that each style carries with it an inherent bias toward some sectors and away from others. Our recent piece, Value Style’s 100-Year Flood, highlighted the significant role that sector weights (overweight Financials and Energy, underweight Technology) played in Value’s decade-long stretch of underperformance.

Real Rates and the Federal Deficit

The real short-term interest rate shows how inappropriately-loose monetary policy has remained in the face of a steady economic expansion.

Value Style’s 100-Year Flood

Value is the philosophical cornerstone of many legendary portfolio managers and is widely recognized as one of the most robust quantitative investment factors. Yet, despite its compelling conceptual merits and long-term record of superior returns, recent years’ underperformance of Value has lasted long enough to weigh on even 10-year performance records.

EM Closed-End Fund Discount/Premium: No Longer A Sentiment Factor

Closed-end funds (CEFs) rarely trade at net asset value (NAV). They either trade at a premium or a discount to share price. When demand for underlying assets is high, the price of a CEF will move above its NAV, trading at a premium. On the contrary, when investors are pessimistic about the underlying assets of a CEF, the price is driven below NAV, trading at a discount. Many studies have looked at CEF discounts and premiums as a means to gauge investor sentiment toward the assets they represent.